Definition: The Marginal Cost refers to the change in the total cost as a result of the production of one more unit of the product. In other words, the marginal cost is the increase or decrease in the total cost due to the production of one additional unit of the product.

The marginal cost includes any cost incurred in producing the next unit of the product and hence is expressed as:

MC = ΔTC/ ΔQ

Where,

ΔTC = Change in total cost, ΔQ = change in quantity

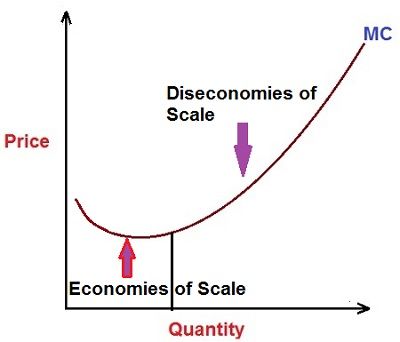

The purpose of marginal cost is to determine the point where the firm reaches its economies of scale. This can be shown in the figure given below:

The marginal cost curve is a U-shaped curve, which shows that cost starts at higher point and declines with the increase in the production. The cost declines with the increase in the level of output because of the economies of scale. When the cost is lower, the firm can hire specialized labor, avail discount benefits on bulk purchase of raw materials, enjoy the full utilization of machines and equipment, etc.

But after some time, the marginal costs starts rising, which shows, the cost increases with the increase in the level of output. This is because the curve reaches the point where diseconomies of scale persist. The costs rise because the resources from the current source might have completely exhausted and the firm purchases raw materials from other sources at a relatively higher price, hire more management, buy more machines and equipment, etc.

Till the price charged for the product is greater than the marginal cost, the revenue will be greater than the added cost and the firm will continue its production. But, as soon as the price charged is less than the marginal cost, the revenue declines, and it is not wise to expand production.

Leave a Reply