Definition: Credit Rating can be defined as the assessment of the ability of the borrower, to discharge their financial obligations. It is an approximation of the creditworthiness of an individual, entity or commercial instrument, considering various factors, representing the capability and willingness, to pay financial commitments in time.

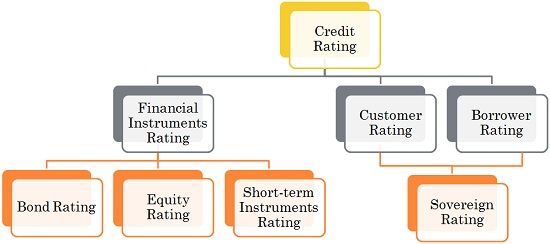

Credit rating is instrument specific and is meant to grade various commercial instruments, with respect to the credit risk and the obligator’s ability to make good the debt obligations, as per the terms of the agreement. The different types of credit ratings are depicted in the figure below:

Simply put, credit rating refers to the expression of opinion concerning debt instrument, based on credit risk evaluation, given by rating agency as on a particular date, indicating the probability of principal plus interest to be met by the borrower in a timely manner. There are three factors which are to be considered during default risk assessment and quality rating, they are:

- Issuers ability to pay.

- Strength of the instrument owner’s claim on the issue.

- Economic importance of the marketplace of the issuer.

Expression of Credit Rating is in alphabetical or alphanumerical symbols, that enables the investor to distinguish the debt instruments, as per their underlying credit quality.

Steps Involved in Credit Rating

- Request from issuer and analysis: The first step to credit rating is that the enterprise applies to the rating agency for the rating of a particular instrument. Thereafter, an expert team interacts with the firm’s those charged with governance and acquires relevant data. Factors which are considered includes:

- Historical performance

- Financial Policies

- Business Risk profile

- Competitive Position, etc.

- Rating Committee: Based on the information gathered and evaluation performance, the presentation of the report is made by the expert’s team to the Rating Committee, in which the issuer is not permitted to take part.

- Communication to management and appeal: The decision of the rating is shared with the issuer and if he/she does not agree with the decision, then an opportunity of being heard is given. The issuer is required to provide material information, so as to appeal against the decision. The decision is reviewed by the committee, but that does not make any change in the ratings.

- Pronouncement of the rating: When the issuer agrees to the rating decision, the agency make a public announcement, of the rating.

- Monitoring of the assigned rating: The agency which rates the issue, overlooks the performance of the issuer and the business environment in which it operates.

- Rating Watch: On the basis of continuous critical observation undertaken by the rating agency, it may place a rated security on Rating Watch.

- Rating Coverage: Credit Ratings are not confined to particular debt instruments, but also covers public utilities, transport, infrastructure, energy projects, Special Purpose Vehicles etc

- Rating Scores: Rating scores are given by the credit rating agencies like CRISIL, ICRA, CARE, FITCH.

Credit Rating is of great help, not just in investors protection but to the entire industry, as it directly mobilizes savings of the individuals.

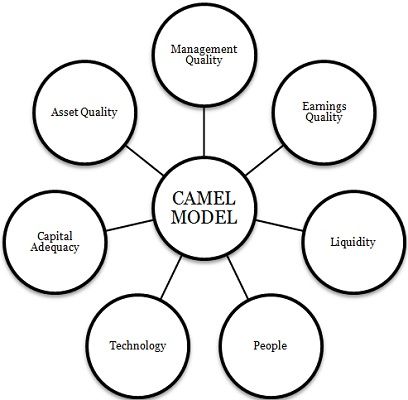

CAMEL Model

CAMEL rating expands to:

- Capital: Capital structure, i.e. retained earnings and external funds raised, fixed dividend for Preferred stockholders and fluctuating dividend for common stockholders and adequacy of long-term debts adjusted to gearing level.

- Assets: Revenue earning capacity of the assets which are in use or to be used, fair values, obsolescence, consistency, methods of depreciation etc.

- Management: The degree to which management personnel is involved, authority, teamwork, timeliness, appropriateness of decision-making and so on.

- Earnings: Stability, trends, absolute levels, adaptability to cyclical fluctuations, the firm’s capability to discharge debts.

- Liquidity: Corporate policies for stock and creditors, the effectiveness of working capital management, etc.

The parameters discussed above are the key basis for determining the creditworthiness of an issuer, which results in the rating of a debt instrument.

Leave a Reply