Definition: In the general sense, the budget is described as a precise statement, representing a financial estimate of income and expenditure of the government for a certain period. In cost accounting, budget means a quantitative statement, prepared before a particular period to serve as an estimate of future receipts and disbursements.

The integrated process of preparing, implementing and operating budgets is called as Budgeting.

Features of Budget

- It is an estimate of the economic activities of an entity which related to a specified future period.

- It must be written and approved by the appropriate authority.

- It should be modified or corrected, whenever, there is a change in circumstances.

- It plays the role of a business barometer that helps in measuring the performance of the business by comparing actual and budgeted results.

- It is prepared on the basis of past experiences and trends in the business.

- It is a business practice, which is used to forecast the operating activities and financial position of the business.

Budget is used to fix targets in monetary terms and control the deviations if any. Further, it can also be used as a basis to measure the performance of the organization.

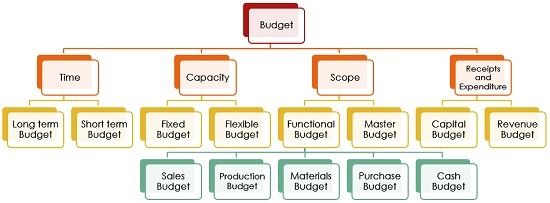

Classification of Budgets

- Based on time

- Long-term Budget: The budget designed by the management for a long-term, i.e. three to ten years is called as long-term budget.

- Short-term Budget: As the name suggests, the budget which is prepared for a period ranging from 1 to 2 years, is called short-term budget.

- Based on Capacity

- Fixed Budget: The budget created for a fixed activity level, i.e. the budget remains constant regardless of the level of activity, is called as fixed budget.

- Flexible Budget: The budget which changes with the change in the level of activity is a flexible budget. It identifies the fixed cost, semi-variable cost and variable cost, to show the expected results at different volumes.

- Based on Scope

- Functional Budget: The budget which is concerned with the business functions is called as functional budget. It can be further classified as:

-

- Sales Budget: Sales budget is used to determine the quantity of anticipated sales and the expected selling price per unit.

- Production Budget: It is prepared to indicate the production for the specified period and is expressed in the units of outputs produced.

- Materials Budget: The budget prepared to show the quantities of direct material and raw material required to manufacture the finished product.

- Purchase Budget: Purchase budget is designed to estimate the quantity and value of different items to be bought at different points of time, considering the production schedule and inventory required.

- Cash Budget: The budget highlights the cash needed by the business in a specified period, taking into account all the receipts and payments of the business.

Apart from those discussed above, there are other functional budgets also, i.e. plant utilization budget, direct material usage budget, factory overhead budget, production cost budget, cost of goods sold budget, selling and distribution cost budget, administration expenses budget, etc.

-

- Master Budget: Once all the functional budgets are created, then the financial officer will prepare a master budget. It is an integrated budget that reflects the estimated profit and loss and financial position using Budgeted Profit & Loss Account and Budgeted Balance Sheet of the concern.

- Functional Budget: The budget which is concerned with the business functions is called as functional budget. It can be further classified as:

- Based on Receipts and Expenditure

- Capital Budget: The budget takes into account the estimated capital receipts and expenditure of the business for a specified period.

- Revenue Budget: The budget that covers all the revenue receipts and expenses of a particular financial year is a revenue budget.

A budget acts as a map for the future economic activities of the business, which are prepared as per the policies of the different organizational functions. It aims at making optimum utilisation of the capital and other resources of the organization.

Juvana joseph says

It really helped me…thank u…

Nwadinobi Marcel says

it really helpful, but i need to reference this page. i couldn’t find any year of publication.

Surbhi S says

It is created on 8 March 2018

Dona says

It is so useful for my studies. Thank you

Nezala F Khoriyo says

This has really helped me as I am preparing to write my Financial analysis exam

QARIBULLAH SHARIFF BAITA says

Indeed you help me also I’m learn alot thing goodly thanks

Ahmey says

Thank you so much 😘

umer farooq says

its good for my exam preparation thank you

nonqubeko nxumalo says

god this is very much helpful

Dharshan says

clear and brief explanation . can be easily understood!