Definition: Insurance refers to a contractual arrangement in which one party, i.e. insurance company or the insurer, agrees to compensate the loss or damage sustained to another party, i.e. the insured, by paying a definite amount, in exchange for an adequate consideration called as premium.

It is often represented by an insurance policy, wherein the insured gets financial protection from the insurer against losses due to the occurrence of any event which is not under the control of the insured.

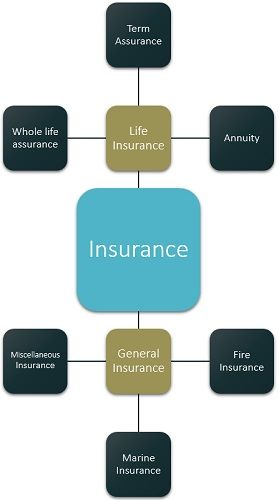

Types of Insurance

Basically, there are two types of insurance, as presented below:

- Life Insurance: The insurance that covers the risk of the life of the insured is called Life insurance. In this, the nominee will get the policy amount, upon the death of the insurer. This is also called as an Assurance, as the event, i.e. death of the insured is certain. The payment of the policy amount on the maturity will be made in one shot (lump sum) or periodical instalments, i.e. annuity.

- Whole life Assurance: Whole life assurance, is one in which the policy amount becomes due for payment on the death of the insured.

- Term Life Assurance: The insurance policy in which the amount has to be paid on the maturity of the specified term, for instance, 10 years or 15 years, then it is called as term insurance policy.

- Annuity: When the policy gets matured, the amount is paid in regular instalments, rather than in lump sum.

- General Insurance: Any insurance apart from life insurance comes under general insurance. In this type of insurance, the policyholder gets the compensation only when the loss is caused to him, due to the reasons indicated in the policy. It is also called as non-life insurance. It is classified into three categories:

- Fire Insurance: A contractual arrangement in which the insurer promises to indemnify the loss caused to the goods and property of the insured due to fire, up to an agreed amount.

- Marine Insurance: When in an insurance contract, the insurer undertakes to compensate the ship or cargo owner against the risks associated with the marine adventure, it is called as marine insurance. It is further divided into cargo insurance, hull insurance and freight insurance.

- Miscellaneous Insurance: Apart from those discussed above, there are other types of general insurance business which cover different types of risks. It includes burglary insurance, credit insurance. Motor vehicle insurance, loss of profit insurance, fidelity insurance etc.

The life insurance and general insurance differ in the way that life insurance covers the life risk, whereas general insurance does not cover the risk of life. Secondly, the premium is paid at regular intervals in life insurance, but in general insurance, the premium is paid in lump sum for the year.

Principles of Insurance

- Principle of Uberrimae Fidei (Utmost good faith)

- Principle of Indemnity

- Principle of Insurable Interest

- Principle of Subrogation

- Principle of Causa Proxima (Nearest Cause)

- Principle of Contribution

- Principle of Loss of Minimization

Insurance is a great way to avoid the loss or shift it to another party. It also gives a sense of security to the individuals. Indeed, it mobilises savings of the individuals in the form of investment in the policies, which are reinvested by the insurance companies in the securities of the publicly listed companies, to earn a dividend on it.

Pasha says

Nice post, I like it.

Josh @ Insured Person says

Nice article!

It would be nice if you add information about methods of insurance.

guma tyson says

good work

realesson says

Best Information……. Great Website.

Arthur says

Good article, thank you