Definition: Depreciation is the reduction in the utility of the fixed asset like plant & machinery, furniture & fixtures, vehicles, buildings, etc. because of obsolescence through technology or market conditions, natural wear and tear, the passage of time, exhaustion of subject matter and so on.

Depreciation is a measure which calculates loss in the value of the non-current asset. It is an accounting convention which allocates the cost of depreciable assets over its useful economic life, to ensure that a fair proportion of depreciable amount is written off every year.

Depreciable Asset

Depreciable assets mean, the assets whose expected useful life is limited but are expected to provide their services for more than one accounting year and are held by the company for the purpose of production or administration rather than resale.

Scrap Value

Every asset has some scrap value, also known as residual value, i.e. the amount at which the asset can be resold at the end of its expected useful life. Therefore, the amount charged as depreciation should be such that it will reduce the book value of the depreciable asset to its residual value, at the end of its useful life.

Objectives of Charging Depreciation

- It is charged to ensure that there is a proper estimation of business income.

- The value of fixed assets, net of depreciation shows the true financial position of the enterprise.

- To generate adequate funds in the business, for replacing the assets, after it becomes obsolete.

- It is charged to determine the actual cost of production.

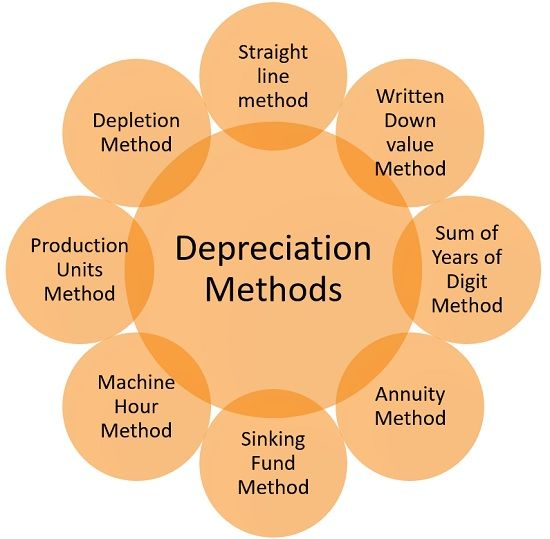

Methods of Providing Depreciation

There are a number of methods of depreciation which are explained as under:

- Straight Line Method: Also known as Fixed Installment Method, an equal amount is charged as depreciation every year throughout the working life of the asset, with the view of reducing the cost of the asset to zero, at the end of its economic life.

- Written Down Value Method: In this method, a fixed percentage of the written down value of the depreciable asset is charged as depreciation, so that the value of the asset equals its break-up value at the end of its working life. This method is also known as the diminishing value method, reducing balance method.

- Sum of Years of Digit Method: This method is a variation of written down value method and is used to accelerate the depreciation.

- Annuity Method: This method is mainly concerned with the cost recovery and a uniform rate of return on any depreciable asset. In the annuity method, along with the value of the asset, interest lost over its life is also written off.

- Sinking Fund Method: Under this method, a certain amount is written off as depreciation every year and placed to the credit of sinking fund account. Further, Government Securities are purchased with the equivalent amount and the interest received, is reinvested and credited to the sinking fund account.

- Machine Hour Method: When a record of actual running hours of each machinery is kept, the calculation of depreciation is based on hours, machines worked.

- Production Units Method: In this method, the depreciation is ascertained by making a comparison of actual production with the estimated production.

- Depletion Method: As the name suggests, the depletion method is used when there is the exhaustion of natural resources like oil reserves, coal deposits and so on.

Depreciation is a non-cash expenditure, and so, it does not result in cash outflow from the business. Moreover, it does not create funds rather it highlights the fact that a fixed amount should be retained from the profits, for the replacement of asset, to continue operations.

Leave a Reply