Definition: Factoring implies a financial arrangement between the factor and client, in which the firm (client) gets advances in return for receivables, from a financial institution (factor). It is a financing technique, in which there is an outright selling of trade debts by a firm to a third party, i.e. factor, at discounted prices.

Factoring is a financial alternative, in financing and management of account receivables. It states the terms and conditions of the sale in the factoring agreement.

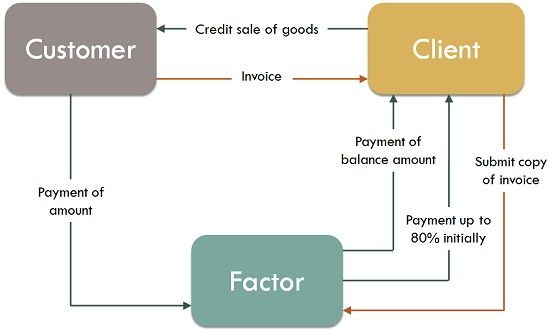

In finer terms factoring is a relationship between the factor and the client, in which the factor purchases the client’s account receivables and pay up to 80% (sometimes 90%) of the sum immediately, at the time of entering into the agreement. The factor pays the balance sum, i.e. 20% of the amount which includes finance cost and operating cost, to the client when the customer pays the obligation.

Types of Factoring

- Recourse and Non-recourse Factoring: In this type of arrangement, the financial institution, can resort to the firm, when the debts are not recoverable. So, the credit risk associated with the trade debts are not assumed by the factor.

On the other hand, in non-recourse factoring, the factor cannot recourse to the firm, in case the debt turn out to be irrecoverable.

- Disclosed and Undisclosed Factoring: The factoring in which the factor’s name is indicated in the invoice by the supplier of the goods or services asking the purchaser to pay the factor, is called disclosed factoring.

Conversely, the form of factoring in which the name of the factor is not mentioned in the invoice issued by the manufacturer. In such a case, the factor maintains sales ledger of the client and the debt is realized in the name of the firm. However, the control is in the hands of the factor.

- Domestic and Export Factoring: When the three parties to factoring, i.e. customer, client, and factor, reside in the same country, then this is called as domestic factoring.

Export factoring, or otherwise known as cross-border factoring is one in which there are four parties involved, i.e. exporter (client), the importer (customer), export factor and import factor. This is also termed as the two-factor system.

- Advance and Maturity Factoring: In advance factoring, the factor gives an advance to the client, against the uncollected receivables.

In maturity factoring, the factoring agency does not provide any advance to the firm. Instead, the bank collects the sum from the customer and pays to the firm, either on the date on which the amount is collected from the customers or on a guaranteed payment date.

Based on the factoring type, the collection of the debt is performed by the factor or the client, as the case may be.

Procedure

- Borrowing company or the client sells the book debts to the lending institution (factor).

- Factor acquires the receivables and extend money against the receivables, after deducting and retaining the following sum, i.e. an adequate margin, factor’s commission and interest on advance

- Collection from the customer is forwarded by the client to the factor and in this way, the advance is settled.

- Other services are also provided by the factor which includes:

- Finance

- Collection of debts

- Maintenance of debts

- Protection of Credit Risk

- Maintenance of debtors ledger

- Debtors follow-up

- Advisory services

The factor gets control over the client’s debtors, to whom the goods are sold on credit or credit is extended and also monitors the client’s sales ledger.

Leave a Reply