Definition: Lease is a financial arrangement, wherein one party (lessor) allows another party (lessee) to use the capital asset or equipment for a definite period, in return for an adequate consideration, i.e. lease rental charges.

In this contract, the lessee need not buy or own the asset in order to use it, because it is a form of renting assets.

Parties to Lease

- Lessor: Real owner of the asset, who can be an individual or firm. The lessor grants the right to use the asset, for a fixed consideration over the period of lease.

- Lessee: The one who legally acquires the right to use the asset or equipment on the payment of recurring rentals which are to be paid over the term of the lease.

There are certain terms and conditions in the contract that exists between the parties, which are written in a legal document called as a lease agreement.

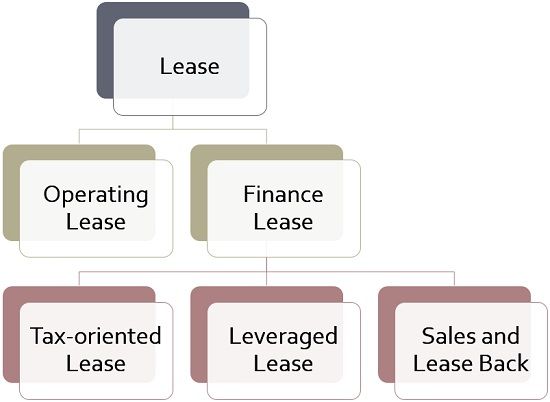

Types of Lease

Basically, there are two most important forms of a lease, i.e. operating lease and finance lease:

- Operating Lease: When in a lease contract, the lessor has the right to get the possession of the asset back from the lessee, at the end of the lease term, then it is called as an operating lease.

- Finance or Capital Lease: When in a lease agreement, lessee retains the possession of the leased asset or equipment even after the period expires then such a type of lease is called as Finance Lease.

This is so because the lease rental charges are set in a way that the whole price of the leased equipment or asset along with the return on investment is recovered to the lessor, within the term, by way of rentals.

- Tax Oriented Lease: When in a lease contract, for the purpose of claiming tax benefit of depreciation, the lessor is regarded as the owner of the asset, then this type of lease is called as a tax-oriented lease.

Further, the amount of depreciation is deducted from lease rentals, which results in the reduction of profit to the lessor.

- Leveraged Lease: It is the type of tax-oriented lease, in which a certain amount is taken as a loan by the lessor from the lender to buy the asset or equipment for leasing.

An arrangement is made through a tripartite agreement between lessor, lessee and the lender, wherein if the lessee defaults in discharging the debts, i.e. lease rentals, the lessor will not be held liable to repay the loan, rather the two parties, as in the lessor and the lender can take legal steps to recover the remaining amount due, from the lessor.

- Sale and Lease-Back: A lease arrangement wherein the asset or equipment is sold by the entity to another party, but later on it is taken back from that party, under the lease arrangement.

In this type of lease, the ownership is transferred, but the possession lies with the real owner (lessee), who pays the consideration at periodical intervals to the new owner (lessor).

- Tax Oriented Lease: When in a lease contract, for the purpose of claiming tax benefit of depreciation, the lessor is regarded as the owner of the asset, then this type of lease is called as a tax-oriented lease.

Leasing is an alternative to actually buying the asset, which makes it a low-cost one. Further, it provides a tax benefit of depreciation, which saves taxes.

Shirish Khaire says

Overall this was helpful. Thanks.