Definition: Marginal Costing is a costing technique wherein the marginal cost, i.e. variable cost is charged to units of cost, while the fixed cost for the period is completely written off against the contribution.

The term marginal cost implies the additional cost involved in producing an extra unit of output, which can be reckoned by total variable cost assigned to one unit. It can be calculated as:

Marginal Cost = Direct Material + Direct Labor + Direct Expenses + Variable Overheads

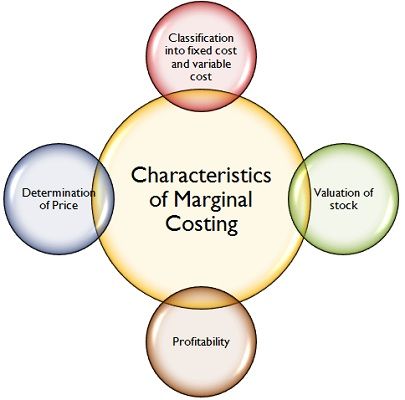

Characteristics of Marginal Costing

- Classification into Fixed and Variable Cost: Costs are bifurcated, on the basis of variability into fixed cost and variable costs. In the same way, semi variable cost is separated.

- Valuation of Stock: While valuing the finished goods and work in progress, only variable cost are taken into account. However, the variable selling and distribution overheads are not included in the valuation of inventory.

- Determination of Price: The prices are determined on the basis of marginal cost and marginal contribution.

- Profitability: The ascertainment of departmental and product’s profitability is based on the contribution margin.

In addition to the above characteristics, marginal costing system brings together the techniques of cost recording and reporting.

Marginal Costing Approach

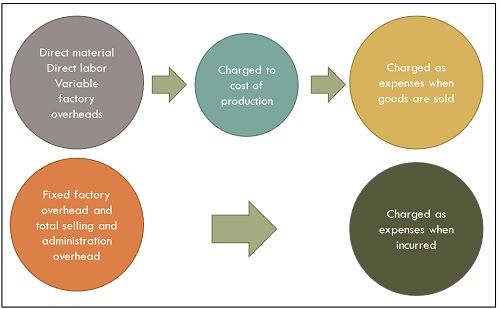

The difference between product costs and period costs forms a basis for marginal costing technique, wherein only variable cost is considered as the product cost while the fixed cost is deemed as a period cost, which incurs during the period, irrespective of the level of activity.

Facts Concerning Marginal Costing

- Cost Ascertainment: The basis for ascertaining cost in marginal costing is the nature of cost, which gives an idea of the cost behavior, that has a great impact on the profitability of the firm.

- Special technique: It is not a unique method of costing, like contract costing, process costing, batch costing. But, marginal costing is a different type of technique, used by the managers for the purpose of decision making. It provides a basis for understanding cost data so as to gauge the profitability of various products, processes and cost centers.

- Decision Making: It has a great role to play, in the field of decision making, as the changes in the level of activity pose a serious problem to the management of the undertaking.

Marginal Costing assists the managers in taking end number of business decisions, such as replacement of machines, discontinuing a product or service, etc. It also helps the management in ascertaining the appropriate level of activity, through break even analysis, that reflect the impact of increasing or decreasing production level, on the company’s overall profit.

Suffering student says

Awesome I got what I was searching for. Thanks, alot 🙂 .

Adrine says

Thanks for informing us

a student says

the data was informative & of simple language

Student says

Awesome I got what I was searching for. Thanks, a lot 🙂 .

The data was informative & of simple language

Kumban Friday says

Am grateful I got what I’m been searching for.. thanks

vicky student says

thanks this was really helpful however I am unsure as to how to cite as this has no author or date, please can you help?

Surbhi S says

“Marginal Costing” businessjargons.com Created on Mar 11, 2017, by Surbhi S. < https://businessjargons.com/marginal-costing.html >

Khushkaran singh says

Well explained from examination point of view

Prashanth Cheruku says

Dear

Thanks for providing precious information

It was very easy to understand the conceptual subject

Warren says

Easy to understand. Thank you

Gladys says

Thanks for it was well explained therefore making it easy to understand

Sourabh Saini says

That was really helpful

Mohamed Bangura says

This site is really helpful

Please help with information regarding calculations about the closing stock