Definition: The term partnership, is used to mean a business structure wherein two or more individuals, come together for undertaking a lawful business and have agreed to share the profits and losses arising from it. The management and operation of the business should be performed either by all the partners or any of them, acting for all the partners.

The Partnership is the relation which subsists between individuals, who have decided to pool their money, skill and resources in business, to share profits and losses, in an agreed ratio. The members of a partnership, are jointly known as the partnership firm and severally known as partners.

In India, it is governed by the Indian Partnership Act, 1932 and is formed as per the provisions of the act. It is started through a legal agreement between partners, called as partnership deed. It lays down the terms and conditions regulating partnership, such as profit and loss sharing ratio, nature of the business, duration of business, duties and obligations of partners, capital contributed by each partner, manner of conducting business and so on.

Characteristics of Partnership

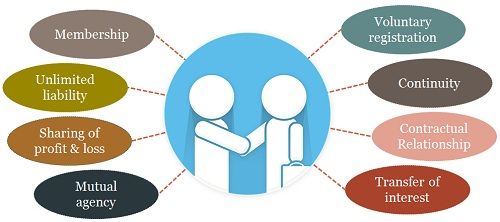

- Membership: At least two persons are required to begin a partnership while the maximum number of members is limited to 100. Further, all the individuals entering into partnership must be legally competent to do so, as they have to enter into a contract to become partners. Thus, minors, insolvent and lunatic persons cannot become members, but a minor can be admitted to partnership, to share profits.

- Unlimited liability: The members of a partnership have unlimited liability, i.e. they are collectively and individually liable for the firm’s debts and obligations. So, if in case business assets are not adequate to repay liabilities, personal assets of all or any partner can be claimed by the creditors to realise the outstanding amount.

- Sharing of profit and loss: The main purpose of the partnership is to share profit in the agreed ratio. However, in the absence of any agreement between partners, the business profits or losses are divided equally among all the partners.

- Mutual Agency: The partnership business is undertaken by all the partners or any of the partner, who acts on behalf of all the partners. So, every partner is a principal as well as an agent. Further, the acts of partners bind each other as well as the firm.

- Voluntary Registration: The registration of partnership is not mandatory, but it is recommended, as it offers certain benefits, e.g. in case of any conflict among partners, any partner can file suit against other partner or if there is any dispute between firm and outside party, then also the firm can file a case against that party.

- Continuity: There is a lack of continuity in partnership, like death, bankruptcy, retirement or insanity of any partner can lead the partnership to end. Although, if the remaining partners want to continue operations, they can do so by a fresh agreement.

- Contractual Relationship: The relation subsisting between partners is due to the contract, which may be oral, written or implied.

- Transfer of interest: Mutual consent of all the partners is a must for transferring the interest in the firm to any external party.

In a partnership, the decision making is done with the mutual consent of all the partners. They share among themselves the decision making and control of the regular business operation.

Types of Partnership

- By duration:

- Partnership at will: Partnership existing as per the will of the partners.

- Particular partnership: When the partnership is created, to carry on a certain project, for a specified time.

- By liability:

- General Partnership: Partnership in which partners have unlimited and joint liabilities. All the partners can take part in the management, and they are bound by the acts of one another as well as of the firm.

- Limited Partnership: The type of partnership in which except one partner all the partners have limited liability.

This form of business organisation is easy to set up because it does not require any fees or process. In addition to this, partners enjoy tax benefit, as in, the profit earned or loss incurred by the business pass through to the partner’s personal income tax return.

DENIS says

SO NICE DETAILS

obednego says

That information was really helpful

Hithan gowda says

very helpful

Busubiri Isaac Bill says

job well done

Uche miracle says

Thanks, it’s really helpful