Definition: Audit evidence refers to the information gathered or recorded by the auditor while performing the audit work to form a conclusion on each element, on which the opinion is based. For obtaining audit evidence, a number of audit procedures are applied by the auditor.

It is the duty of the auditor to give an opinion on the financial statements presented by the company and which is all about judgment.

Audit evidence so collected must be sufficient and competent and in appropriate quality, only then the auditor will express his opinion. It comprises source documents and accounting records elemental to financial statements and authenticating information from different sources.

It helps in forming an opinion regarding the financial statements of the company, i.e. if the statements are free from material misstatements, present true and fair view, and are prepared in accordance with the financial reporting framework which is applicable. Also, when the findings of the auditor are disputed, this evidence supports the opinion of the auditor.

The term ‘evidence’ may cover all those items that can have an impact on the auditor’s mind, which may affect his opinion concerning the true and fair view of the documents submitted.

Components of Audit Evidence

- Information in Accounting Records: Information contained in different accounting records such as Journal Registers, Ledgers, Invoices, Vouchers, etc. on which financial statements of the company rely.

- Other information: It may include confirmation from external parties and reports from experts.

Nature of Audit Evidence

The formation of opinion by the auditor is based on sufficient and appropriate audit evidence, which are gathered by carrying out the Risk Assessment Procedure and audit procedures i.e. substantive procedure and compliance procedure.

- Sufficient: It indicates the quantum of audit evidence, i.e. how much audit evidence is required to be obtained. This mainly depends on the size and scale of the business.

- Appropriate: It indicates the quality of audit evidence, i.e. how relevant and reliable the audit evidence is. This depends on the source from which the evidence is obtained.

Factors Influencing Auditor’s Judgement on Audit Evidence

The sufficiency and appropriateness of audit evidence are influenced by the following factors:

- The materiality of the item

- Type of availability of information

- Experience gained during the earlier audit

- Degree of risk of misstatement, be it related to nature of the item, nature of the business conducted, adequacy of internal control, etc.

- Result of audit procedures.

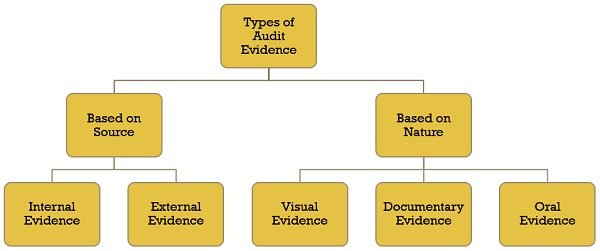

Types of Audit Evidence

On the basis of Source

- Internal Evidence: Evidence collected within the client’s organization, be it books of accounts, management response to any question, etc.

- External Evidence: Evidence collected outside the client’s organization, i.e. any sort of confirmation received from a third party. Example: Bank, Debtor, or Creditor.

On the basis of nature

- Visual Evidence: Evidence in the form of analysis and observations.

- Documentary Evidence: Evidence available in the form of a written document.

- Oral Evidence: Evidence obtained by way of interviewing or inquiry.

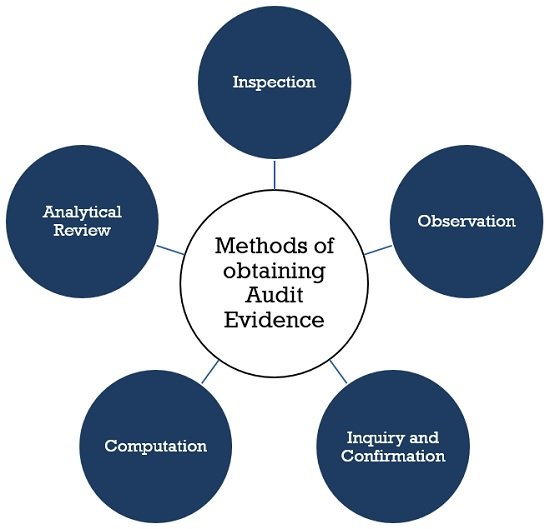

Methods of obtaining Audit Evidence

There are five methods of obtaining audit evidence which is explained in the points that follow:

- Inspection: Inspection means scrutinizing records, documents, and tangible assets. It provides audit evidence of the different degrees of reliability.

- Observation: In this method the auditors witness the process being performed by the auditee staff. For example Physical counting of inventory.

- Inquiry and Confirmation: Inquiry is when the auditor’s team seeks the required information from knowledgeable persons within and outside the company. It can be in the form of formal written inquiries, directed to the third-party or informal oral inquiries directed to persons working within the organization.

Confirmation comprises the response to a particular inquiry to authenticate information, contained in accounting records. It is the process of asking for and receiving the relevant information in written form, from a third party, which certifies the validity of the item. - Computation: It is concerned with verifying the arithmetical accuracy of the source documents and accounting records.

- Analytical Review: It involves analyzing significant ratios and trends of the organization and looking for any unusual fluctuations and items.

A word from Business Jargons

Simply put, audit evidence is the information that the auditor uses to arrive at conclusion, on the basis of which independent opinion can be expressed. It may cover all the information generated by the accounting system, actual physical inspection of assets, documents generated by third parties and within the company, comparison of balances of accounts, etc.

Leave a Reply