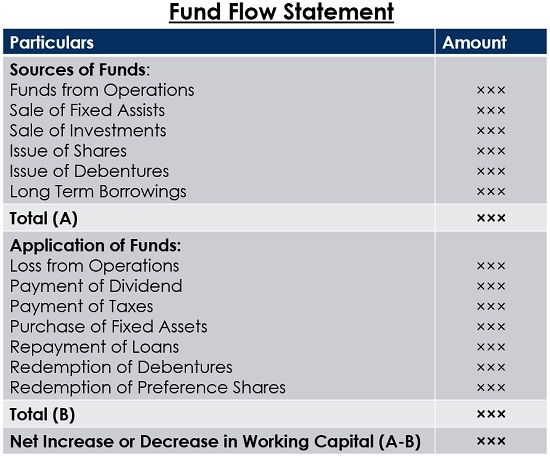

Definition: Fund Flow Statement implies a snapshot of the movement of funds, i.e. inflow or outflows of the firm’s financial assets for a specific period. It represents, “from where the funds are received and where the funds are utilised” by the company during a particular period.

The word ‘fund‘ refers to a sum of money, which is used to finance the firm’s day to day operations and acquire assets for the business. The flow of funds represents the movement of funds, i.e. the change in economic resources, from one asset or liability to another. In this way, the fund flow statement implies a method of analysing the changes in the firm’s financial position, between two balance sheet dates.

Fund flow statement is useful in knowing the changes in the structure of assets, liabilities and capital. It shows whether the sources of funds coincides with its application and indicates the accuracy of a firm’s financing and investment decisions. Unlike the cash flow statement, which is prepared on a cash basis, the fund flow statement is prepared on an accrual basis.

Preparation of Fund Flow Statement

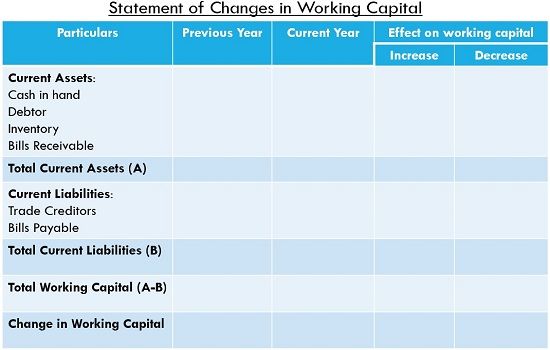

- Step 1: Preparation of Statement of Changes in Working Capital: Statement of Changes in working capital is a summary that shows the net increase or decrease in the working capital of the business.

The working capital of the firm increases if there is an increase in the current assets or decrease in the current liabilities. However, the working capital of the firm decreases if there is a decrease in the current assets and an increase in the current liabilities.

Further, there will be no change in the working capital if there is a realization from debtors or bills receivable or payment made to creditors or bills payable, goods are sold on credit and goods are purchased on credit.

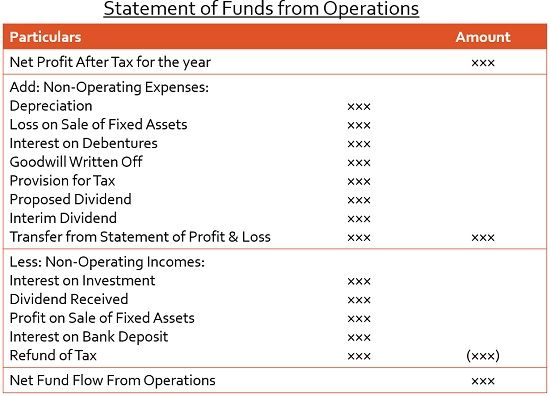

- Step 2: Determination of Funds from Operations: Funds from operations refers to the profit earned or loss incurred from the regular business operation. The ascertainment of funds from the operation is vital for the preparation of fund flow statement.

- Step 3: Preparation of Fund Flow Statement: After recognizing the funds/loss from operations, fund flow statement is prepared, which will show the net increase or decrease in the working capital.

Basically, any change in the assets and liabilities may result in the inflows and outflows of funds, but not always, as in case of depreciation or revaluation of assets, there is no inflow or outflow of funds. Hence, only those assets or liabilities will become a part of the statement, which actually leads to the flows of the fund to/from the business.

Leave a Reply