Definition: In Double entry system, due to its dual aspect, every transaction affects two accounts, one of which is debited and other is credited. To record the transactions in the journal, in a sequential way, certain rules are required, and these rules are called as Golden Rules of Accounting.

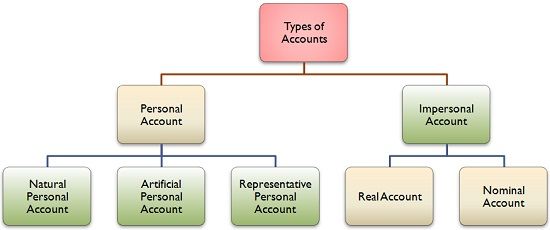

Types of Account

To understand the golden rules of accounting, one should know the types of accounts. Basically, there are two types of accounts, namely:

- Personal Account: Accounts that deals with persons, i.e. human beings and artificial judicial persons such as companies, government organisations, HUF, etc.

- Natural Personal Account: Accounts that are concerned with natural human beings are called natural personal account. It includes accounts of debtors, creditors, proprietor, etc.

- Artificial Personal Account: All the business concern has a separate legal identity in the eyes of the law, and so the entities are different from its members. Therefore, the accounts of clubs, charitable trust, company, bank, etc are covered under this category.

- Representative Personal Account: The accounts which represent persons or group thereof, are called representative personal accounts, such as capital A/c, drawings A/c, prepaid A/c, outstanding liability A/c.

- Impersonal Account: As the name suggests, the accounts which are not personal are called impersonal account.

- Real Account: Real accounts covers all the accounts related to firm’s assets. It includes both tangible real account, such as cash A/c, building A/c, furniture A/c, investment A/c, etc. and intangible real account, such as goodwill A/c, patent A/c, intellectual property A/c.

- Nominal Account: These are fictitious accounts, that are associated with expenses, losses, revenues and gains of the firm, such as rent and rates account, travelling expenses A/c, the commission received A/c, interest paid A/c.

As far as the business transactions are concerned, they are divided into three categories:

- Personal transactions.

- Transactions related to business assets.

- Transactions related to expenses, losses, incomes and gains.

Personal Transactions are recorded in a personal account, transactions concerning assets and properties are covered in real account. Lastly, transactions related to expenses losses incomes and gains are considered in the nominal account. In short, the golden rules of accounting are provided for these three accounts only.

Golden Rules of Accounting

- Personal Account

Debit the Receiver, Credit the Giver - Real Account

Debit what comes in, Credit what goes out - Nominal Account

Debit all expenses and losses, Credit all incomes and gains

Example

- Commenced business with cash Rs. 5,00,000

- Purchased goods from Alex Rs. 25,000

- Sold goods worth Rs. 10,000 to Sam for cash

- Office Rent paid Rs. 12,000

The Golden rules of Accounting are the mainstay of the entire process of accounting. These are the rules for debit and credit, that helps in the preparation and presentation of financial statement in a systematic manner.

Rajez says

Fine…

Rinku negi says

I would like to thanks all about your content which makes very helpful to all of us .

Yogesh Kulkarni says

Excellent content and very good clarity for non-accounting and even accounting professionals!

Thank you

CA Yogesh Kulkarni – Goa