Definition: Income Statement or otherwise called as statement of profit and loss, is the summary prepared by the company’s management, reporting the revenues, expenses, gains and losses for the particular financial year. Simply put, it portrays the final result of the company’s operations over a period.

Income statement forms part of the company’s financial statement along with the Balance Sheet, Cash flow Statement and Statement of Owner’s Equity, which is used to analyse the company’s financial position, performance and profitability. It is a report that lists out and categorizes various items of revenues and expenses, that amounts to net profit or loss for the stated period.

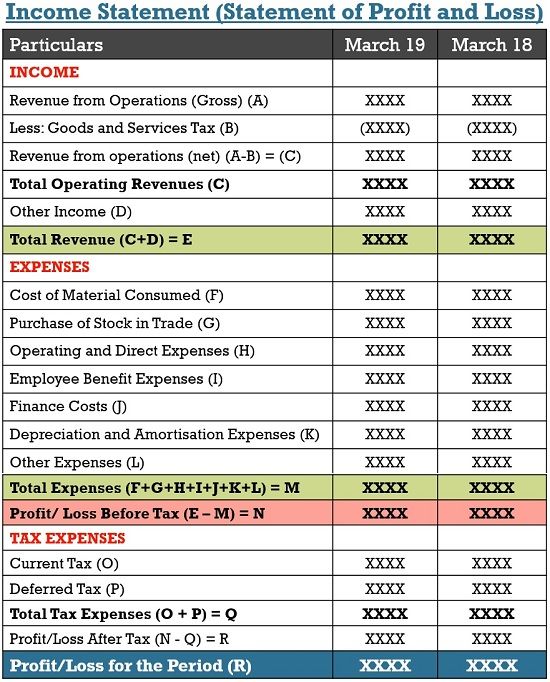

Format of Income Statement

Traditionally income statement is called as Profit and Loss Account, which is further subdivided on the basis of the nature of the concern. If the business entity is engaged in production and manufacturing business, there are three main divisions, i.e. manufacturing account, trading account and profit & loss account.

As against, if it is a trading company, then there are only two divisions, i.e. trading account and profit & loss account.

Components of Income Statement

The income statement is a snapshot of how the company’s operating and non-operating activities contribute to the net income or net profit. And so, it includes only nominal accounts. The major components of the income statement are:

- Operating Revenue: The value received by the enterprise for the goods sold and services rendered to the customers for a particular period less goods and services tax (if any), results in total operating revenue.

- Operating Expenses: Operating Expenses refers to the expenses which are outrightly related to the entity’s regular business operations so as to provide goods and services to customers, i.e. raw materials, wages and salaries, supplies, rents, etc.

- Non-operating Revenue: The amount received from non-core business operations, or from infrequent items are called non-operating revenue, such as dividend income, interest income, commission received etc.

It includes gains, i.e. the profit from selling old assets, scrap material, ancillary business items or investments, at a value higher than its actual value till date. Here, the word ancillary business items refer to those equipment or objects that help in carrying out business operations.

- Non-operating Expenses: The amount incurred on non-core business activities or unusual/infrequent items are non-operating expenses, i.e. interest expenses, restructuring expenses, lawsuit settlement expenses, commission paid, etc.

It covers losses also, i.e. loss on selling the selling old assets, business investments, scrap material, or ancillary business items of the concern at a value lower than its actual value till date, as well as loss from writing down of assets, foreign exchange losses, etc.

Note: Income Statement can be presented in both cash and accrual basis of accounting, however, it should be kept in mind that if there are prepaid expenses and accrued income, income statement reflects higher income in case of accrual basis, but lower in case of cash basis of accounting.

On the other hand, if there is any outstanding expenses or unaccrued income, the income statement shows a lower income in case of accrual basis, but the income will be higher in case of cash basis of accounting.

Basically, income statement acts as a report on the company’s financial health, which is of great use to company’s stakeholders, i.e. business partners, creditors, debtors, investors, suppliers, shareholders and so forth.

Michael says

When someone writes an article he/she maintains the image of a user in his/her mind that how a

user can know it. So that’s why this article is amazing. Thanks!