Definition: In the simplest sense, income tax is a tax imposed on the income of persons, earned by them in the previous year. It is a composite tax on the total of income derived from multiple sources. To compute the tax, income is classified into different slabs and tax is charged as per the rate of the concerned slab. It is majorly classified into:

- Personal Income Tax: It is imposed on the total income of persons like Individuals, HUF, Firms, AOP, BOI etc.

- Corporate Income Tax: It is the tax is charged on the taxable profit of companies and other unincorporated bodies.

Do you know?

In the year 1860, Sir, James Wilson introduced this tax in India for the very first time. He was the first Finance Minister of India. The reason for its imposition is to meet the expenses and losses, which are incurred due to the Revolt of 1857.

Basic Concept

- It is an annual tax on the income of the assessee.

- Income of the previous year is taxable in the immediately following assessment year at the prescribed rates.

- Fixation of the tax rates for the coming financial year takes place through budget every year.

- Every person with income more than the exempted income is liable to pay tax.

- Tax is imposed on the total income of the person whose calculation is as per the provisions of the IT Act 1961.

- The total income of the person is calculated after taking into account the residential status of the assessee. It is classified into five heads:

- Income from salary

- Income from house property

- Profit and gains from business or profession

- Capital gains

- Income from other sources

Why do we pay taxes?

Taxes are the cost that we have to pay for living in a civilized society.

It is one of the major sources of revenue for the government. The IT Department of the Government imposes this tax. The revenue generated from the collection of tax on the income and other taxes is used to:

- Fund public utility services

- Pay government obligations

- Maintain law and order in the country and

- Supply goods to citizens.

The determination of tax liability of the assessee relies on the slabs and rates for different heads.

As per law, the taxpayers need to file an Income Tax Return, depending on their income and the sources from which the income arises. After filing the ITR, the individual will get to know about their tax obligation.

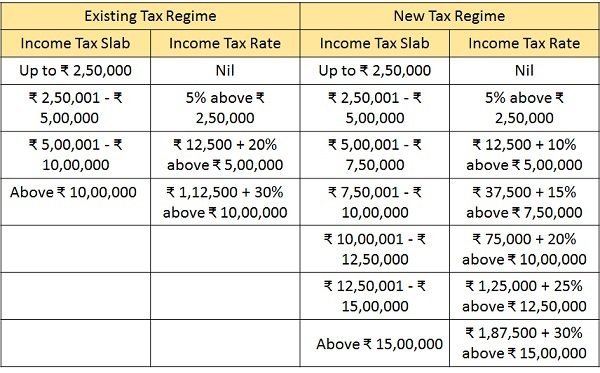

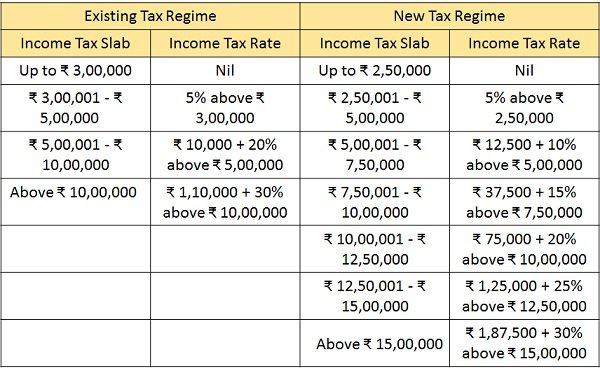

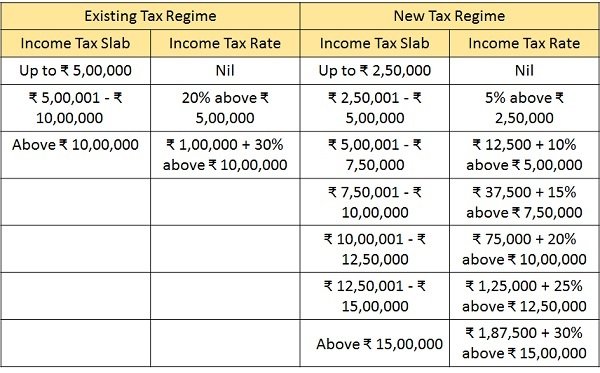

Income Tax Slabs and Rates for Assessment Year 2022-23

Individuals and HUFs can choose the Existing Tax Regime or the New Tax Regime with a lower rate under section 115 BAC of the IT Act, 1961. But, the taxpayer choosing the second option will not be allowed certain Exemptions and Deductions such as 80C, 80D, 80TTB, and HRA available in the Existing Tax Regime.

- Individuals whose age is below 60 years anytime during the previous year (resident or non-resident):

- For Individuals whose age is above, 60 years but below 80 years anytime during the previous year (resident or non-resident):

- For Individuals whose age is above 80 years anytime during the previous year (resident or non-resident):

What are Assessment Year and Previous Year in Income Tax?

The year in which evaluation and taxation of income take place is the assessment year. But that income is earned during the previous year.

What is Income?

Income refers to the monetary inflow, arising from different sources with some degree of regularity or expected regularity.

Rules for ascertaining income

- The existence of a definite source of income is pertinent to bringing a receipt within the net of taxable income.

- The income tax does not make any distinction between legal and illegal income, as both are taxable.

- It is not necessary that income must be received regularly or periodically like weekly, monthly or quarterly or even the amount received in a lump sum can also be called income, provided it is regarded as income taking into account other factors and consideration.

- Receipt of income must be from outside

- Even receipts in kind or services of monetary value are also income.

- From the taxation point of view, whether the income is temporary or permanent is irrelevant.

- Even when the assessee has earned income but has not received it, we will treat it as the income of the assessee as per the act as he was entitled to receive it.

- If under any legal obligation there is a creation of a charge on the assessee’s income, then up to that extent, the amount will be deducted from income.

Who is liable to pay income tax?

All the persons whose total income earned in the previous year is more than the amount exempted from the income tax are liable for the payment of tax. Further, the payment of tax should be on the taxable amount that is more than the exempted amount according to the rates specified under the Act.

Salient Features of Income Tax

- Direct Tax: It is a form of direct tax, as the incidence of the tax falls on the person to whom it is imposed. Hence, one cannot transfer or shift it to any other person.

- Central Government Tax: Because the central government imposes tax on the income it is a central tax.

- Exemption Limit: Exempted income limit is there for all types of assessees. For instance: Exempted income in the previous year 2020-21 for:

- Male/female assessee, who has not attained the age of 60 years and HUF, is 2,50,000

- Senior Citizen assessee who has attained the age of 60 years but below 80 years is Rs. 3,00,000

- Super Senior Citizen assessee who has attained the age of 80 years or more is Rs. 5,00,000

- Firm, Company, Local Body is Nil

- Tax on Net Taxable Income of Previous Year: It is imposed on the assessee’s net taxable income earned in the previous year.

- Computation of Tax as per the existing tax slabs and rates: It is calculated based on various income tax slabs and rates specified by the concerned Finance Act. These slabs and rates are announced every year by the Finance Minister through the budget.

- Income Tax payment in the current assessment year: The assessee pays tax for the income earned in the previous year in the current assessment year. To further understand this, income tax for the previous year 2020-21 is paid in the assessment year 2021-22.

- Progressive Tax Rate: One should take a note that tax is not imposed on all the persons at the same rate, rather it increases with the increase in the income. Thus, the minimum rate of tax is 5%, whereas the maximum rate is 30%.

A word from Business Jargons

In a nutshell, Income tax is a permanent source of income for the government. Also, it encourages savings and investment among people. Further, it removes disparities between the haves and have nots and fills the gap between the two. And that is why we use slab rates.

Leave a Reply