Definition: An auction sale is a public sales event for a property or good in which the bidders are invited to place competitive bids. In this, the bidder who places the highest bid buys the product or property under auction. For this purpose, many prospective buyers arrive at the decided time and venue for participating in the event.

In short, an auction sale refers to the sale of goods by undergoing a bidding process. We read the rules for auction sale under the Sale of Goods Act, 1930.

Execution of the auction sale can take place in an open or closed format. While in an open auction bidder knows about other bids. In a closed auction, the bidders do not have knowledge about the competing bids.

In this, the selling of personal or commercial property or goods takes place. The auctioneer sells it to the highest bidder present at the time. It can take various forms like:

- Selling wholesale stock on an online auction site.

- Holding an auction at a specific place to sell unwanted belongings or settle debts.

Concept of Auction Sale

In an auction sale, goods are offered for bid. This means that all the invited members can take part in the bidding process. In the end, the auctioneer sells the item to the highest bidder.

Of the invited members, the ones who are interested to take part and buy the product are ‘Bidders’. And the price they offer for the item undergoing auction is ‘Bid’.

Considering the Contract Act

- Notice or advertisement of the auction sale is the Invitation to an offer

- Bid accounts for the Offer

- The Fall of the Hammer is the Acceptance of the offer.

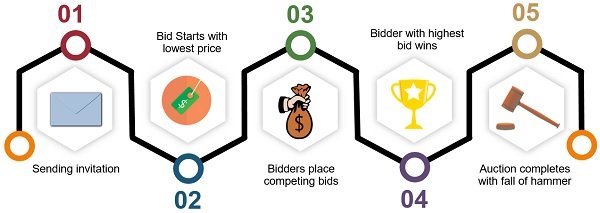

Process of Auction Sale

- The process of auction sale starts with sending an invitation to the parties for auction. For this purpose, circulation of an advertisement and catalogue of the goods under auction along with the terms of sale takes place.

- In this process, the bidders act as competitors and thus they place competing bids. In essence, each subsequent bid is higher in price than the last one.

- When the auctioning begins, the auctioneer starts with the lowest deal price. He does so to gather the attention of most of the bidders. The interested buyers offer bids one after another and seek to outbid each other. And so, with each next bid, the price keeps on increasing until it reaches a point where no other bidder offers a higher price than the last one.

- Therefore, the item goes to the highest bidder present at the time.

- An auction sale is complete when the auctioneer signals it by the Fall of a Hammer or any other customary way. And with the Fall of Hammer, the property in goods passes to the highest bidder. And so, until the fall of the hammer, the bidder can revoke his offer, if he wants to.

- As soon as the vendor accepts the highest bid offered, the auction comes to end. Thereafter, the buyer has to pay the agreed price and take possession.

- After that, the auctioneer can ask for payment of the sale money via cash. The buyer cannot compel the auctioneer to accept payment of money by way of a bill of exchange or cheque.

Point to Note

In every auction sale, an implied warranty exists. The warranty states that the auctioneer has the right to sell and that if he is unaware of the defect in the title of the principal. In such a case, the auctioneer commits to make certain that the buyer gets a quiet and undisturbed possession of the goods.

Rules Relating to Auction Sale

Goods sold in lots

For the goods whose sale takes place in lots, each lot at first instance is regarded as a separate contract of sale.

Time of Completion

As said above, the sale completes when the auctioneer declares its completion by the Fall of Hammer. This fall of a hammer is followed by the words, “one, two, three” and ” going, going, gone”. If the bidder wants to withdraw the bid, he can do so before such an announcement.

Further, the auctioneer can also reject the bid if he feels that the bid is very less than his expectation. It is obvious that rejection of the highest bid damages the business reputation. This is because it is a practice of trade that the goods go to the highest bidder.

Reservation of right to bid

The seller may explicitly reserve his bidding rights in the auction sale. He can do so by notifying it at the time of announcement.

Therefore, the seller or any other person can bid on his behalf, only when the right to bid is reserved by the seller.

No reservation for the right to bid

When the seller does not notify the right to participate in the bid. Both the seller or his representative cannot take part in the bid.

In spite of the absence of any right, if the seller participates in the bid or the auctioneer takes the bid from the seller purposely. Then, the law treats it as illegal. Any sale of this kind made to any person shall enable the buyer to treat it as fraudulent.

Reserved Price

Therefore, the seller has the option to set a reserve price for the goods undergoing auction. Here, a ‘Reserve Price‘ is a price below which the auctioneer won’t sell. If due to any mistake, the auctioneer sells the lot for less than the reserved price, then no valid contract comes into force. Also, he can refuse to deliver the goods to the highest bidder.

For the auction sale without the reserve price, the goods have to be sold highest bidder, regardless of the bid amount.

Revocation

It is a rule that before the acceptance of the offer, the bidder can withdraw it and need not necessarily be accepted.

In this regard, it is worth noting that the auctioneer has got the right to make an auction subject to the conditions of his choice. . Hence, if the auctioneer announces that the biddings cannot be revoked after it is made. In such a condition, the rule regarding the revocation of an offer before its acceptance will not apply.

Pretended Bidding

If the seller uses pretended bidding just to raise the bid value, the law treats it as fraudulent. And, the buyer can avoid the contract on such grounds.

Knockout Agreement

An agreement among the intending buyers wherein they commit not to bid against is a knock-out agreement. Such agreements are not illegal.

A word from Business Jargons

Auction Sale is a process of selling goods wherein the owner invites bids from the general public. In this, the person making the highest of all the bids wins, i.e. the goods are sold to him.

Leave a Reply