Definition: Budgetary control refers to a method of management control and accounting, wherein the budgets are established, by forecasting the activities beforehand to the maximum extent and a constant comparison is made between the actual results and the budgeted figures, so as calculate the variances (if any) and take corrective steps accordingly to ensure the achievement of targets.

Hence we can say that the budget is the cause, and budgetary control is the effect.

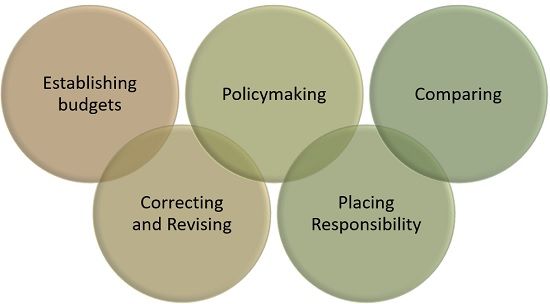

Functions of Budgetary Control

- Setting up of budgets

- Policymaking

- Comparing the actual and budgeted results.

- Taking corrective steps and remedial measures, (if possible) or Revising the budgets (if required).

- Placing responsibility when there is a failure to attain the target.

Budgetary control implies a system that involves an ongoing comparison of the actual performance with the budgets and taking remedial steps immediately, to ensure adherence to the plan.

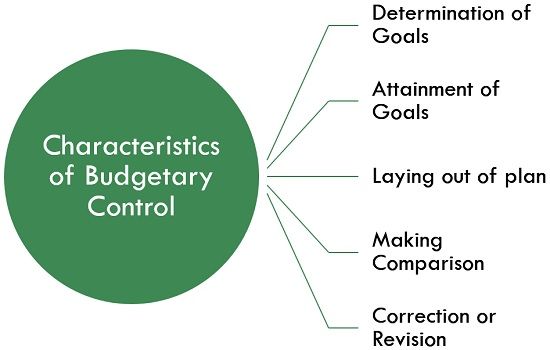

Characteristics of Budgetary Control

- Determination of goals: Budgetary Control helps in ascertaining the goals to be achieved over the accounting period and the policies that are to be implemented for the attainment of these objectives.

- Attainment of goals: It ascertains the range of activities which are to be carried out for the achievement of objectives.

- Laying out of plan: It assists in formulating a plan or sketches out the operations, concerning every stage of activity, both physically and monetarily, for the entire period.

- Making comparison: It establishes a system for comparing the actual performance with the budgeted ones, by every individual, unit or department and ascertains the causes for discrepancies.

- Correction or Revision: Budgetary control makes sure that the required corrective steps will be taken at the right time when there are deviations from the budgeted targets and if that cannot be implemented then the plan is revised considering all the factors.

Budgetary Control aims at prescribing in exact terms what should be done, how it is to be done in future and ensuring that actual performance is in tandem with the budgets.

Objectives of Budgetary Control

- To delineate the objectives of the business with precision and establish the performance targets, for every unit and department of business.

- To define the responsibilities of each supervisor, manager and other personnel, so that every member of the organization knows about his job, rights and duties.

- To provide a benchmark for making a comparison between standard targets and the actual results, and identify the reasons for so, in order to take necessary actions to correct the divergence.

- To make optimum utilization of the organization’s resources in order to increase productivity and profitability.

- To monitor that the firm is not deviated from the path of its long term objectives, without being affected by contingencies.

- to identify where efforts are required to cope with the situation.

- To align the activities of the business, centralizing the control, while decentralising the authority and responsibility to executives, in the business interest.

- To assist in waste elimination, losses during the production and removal of excess costs.

- To provide a logical basis for the revision of present and future policies.

- To formulate plans for long term with maximum accuracy.

In a nutshell, Budgetary control analyses how efficiently managers utilize budgets to manage cost and operations in a particular period. It helps the company’s management in delegating the responsibility to the executives and provide a basis for forecasting, so as to measure the variances between actual and estimated results.

Leave a Reply