Definition: Control is a primary goal-oriented function of management in an organisation. It is a process of comparing the actual performance with the set standards of the company to ensure that activities are performed according to the plans and if not then taking corrective action.

Every manager needs to monitor and evaluate the activities of his subordinates. It helps in taking corrective actions by the manager in the given timeline to avoid contingency or company’s loss.

Controlling is performed at the lower, middle and upper levels of the management.

Features of Controlling

- An effective control system has the following features:

- It helps in achieving organizational goals.

- Facilitates optimum utilization of resources.

- It evaluates the accuracy of the standard.

- It also sets discipline and order.

- Motivates the employees and boosts employee morale.

- Ensures future planning by revising standards.

- Improves overall performance of an organization.

- It also minimises errors.

Controlling and planning are interrelated for controlling gives an important input into the next planning cycle. Controlling is a backwards-looking function which brings the management cycle back to the planning function. Planning is a forward-looking process as it deals with the forecasts about the future conditions.

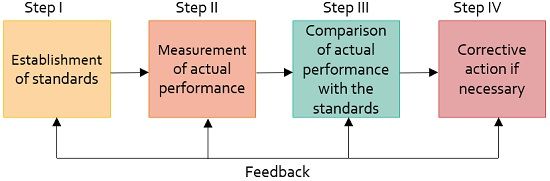

Process of Controlling

Control process involves the following steps as shown in the figure:

- Establishing standards: This means setting up of the target which needs to be achieved to meet organisational goals eventually. Standards indicate the criteria of performance.

Control standards are categorized as quantitative and qualitative standards. Quantitative standards are expressed in terms of money. Qualitative standards, on the other hand, includes intangible items.

- Measurement of actual performance: The actual performance of the employee is measured against the target. With the increasing levels of management, the measurement of performance becomes difficult.

- Comparison of actual performance with the standard: This compares the degree of difference between the actual performance and the standard.

- Taking corrective actions: It is initiated by the manager who corrects any defects in actual performance.

Controlling process thus regulates companies’ activities so that actual performance conforms to the standard plan. An effective control system enables managers to avoid circumstances which cause the company’s loss.

Types of control

There are three types of control viz.,

- Feedback Control: This process involves collecting information about a finished task, assessing that information and improvising the same type of tasks in the future.

- Concurrent control: It is also called real-time control. It checks any problem and examines it to take action before any loss is incurred. Example: control chart.

- Predictive/ feedforward control: This type of control helps to foresee problem ahead of occurrence. Therefore action can be taken before such a circumstance arises.

In an ever-changing and complex environment, controlling forms an integral part of the organization.

Advantages of controlling

- Saves time and energy

- Allows managers to concentrate on important tasks. This allows better utilization of the managerial resource.

- Helps in timely corrective action to be taken by the manager.

- Managers can delegate tasks so routinely chores can be completed by subordinates.

On the contrary, controlling suffers from the constraint that the organization has no control over external factors. It can turn out to be a costly affair, especially for small companies.

Shuvangkar dash says

very nice website and i want to learn many things

Manjeet Kaur says

Awesome got the exactly correct words for each and every topic

Joel says

wow your information was so helpful and grate. thanks so much

MUGALU MANISULI says

This site helped me prepare for my management paper.

Am so grateful.

Labiga Luka says

This is a wonderful site. This side helps me prepare for my exams…thanks, guys.

Abdul sami says

Very interested information

Mizz says

Controlling is tbe aspect for management.

A. Theoretical

B. Practical

C. Mental

D. Physical

Plss answer

Shahid malik says

practical

Akbar Ali says

awesome, this is very helpful and effective content containing website. keep it up

Mwatha says

My understanding and interest in Management have been sharpened by this intellectually thrilling site. You have taken this to the highest level possible. It’s on point.

Sarah says

I managed to do my assignments with clear English. Thank you

Priscilla john says

Please can you difference between cybernetic and non-cybernetic controls

Lega says

This website is great. It has provided the aid I needed and clarification on specific points which were ambiguous. Keep up the good work. Great job, thumbs up.

Syeda says

Helped alot in preparing for exams

Salama says

Thanks alot a very gud site I hv got what I wanted with clear en simple English explanations! I really appreciate you that.

Zaharadeen aliyu says

I really appreciate and happy of this and I like it

Aina Niipindi Andreas says

thanks very much this just made it clear and i got all what i wanted.

gorety akoth says

The site is very fine for revision🥰

Debasmita Roy says

Amazing.. it helped me.

Srinivasa says

Thank you very useful to me and thank you

Mohd Arsh says

It’s really good work

That website has helped me to study keep it up.

Aleeshart says

Wow!! that’s great thank you, it guide me in my presentation excellently

Ijeoma Ann says

This helped me in writing my thesis.

Om prakash yadav says

That’s awesome

PEAFOWL says

This site is so great and wise thanx for your support

Kofi Kissi says

Very amazing site. Kudos to the developers.

sagar badal says

Very amazing site

Sofia says

This content was very useful for me to prepare for exams. The words are easy to study. This is helpful for me. Thanks for making this presentation keep going🖖

Ingrid I Paulus says

This site helped me to finish my assignment.

Indhu says

Good site … Very useful for me

VALENTIN says

Thank you you have good website so much i leant much more here