Definition: Standard Costing is a costing method, that is used to compare the standard costs and revenues with the actual results, in order to arrive at the variances along with its causes, to inform the management about the deviations and take corrective measures, for its improvement.

The term ‘standard cost’ can be defined as the expected cost per unit of the products produced during a period, which is based on various factors. It aims at measuring the performance, controlling the deviations, inventory valuation and deciding the selling price of the product especially when quotations are prepared.

The three main elements of standard cost are Direct Material Cost, Direct Labor Cost and Overheads.

Need of Standard Costing

- Future cost estimation: Standard Costs are determined after considering all the possibilities that may arise in the future. It also helps in deciding whether a particular project is to be undertaken, by determining its profitability.

- Performance check: Standard cost acts as targets to the cost centres which should not be transcended. In such a situation, these targets are helpful in checking the performance through comparison with the actual results.

- Budgeting: The standard costs are used to prepare budgets, and evaluate the performance of the executive staff on the basis of these budgets.

The basic objective of standard costing is to measure the differences between standard costs and actual costs, and analysing them to maintain the productivity of the organization.

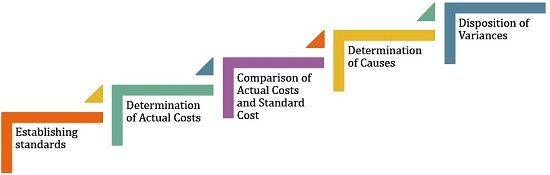

Process of Standard Costing

- Establishing Standards: First and foremost, the standards are to be set on the basis of management’s estimation, wherein the production engineer anticipates the cost. In general, while fixing the standard cost, more weight is given to the past data, the current plan of production and future trends. Further, the standard is fixed in both quantity and costs.

- Determination of Actual Cost: After standards are set, the actual cost for each element, i.e. material, labour and overheads is determined, from invoices, wage sheets, account books and so forth.

- Comparison of Actual Costs and Standard Cost: Next step to the process, is to compare the standard cost with the actual figures, so as to ascertain the variance.

- Determination of Causes: Once the comparison is done, the next step is to find out the reason for the variances, to take corrective actions and also to evaluate the overall performance.

- Disposition of Variances: The last step to this process, is the disposition of variances by transferring it to the costing profit and loss account.

Standard costing can be helpful in ascertaining the profitability of the business at any level of production. Further, it is also useful in practical management functions, i.e. planning and controlling.

Jatin says

It was a very great article about Standard Costing. By seeing various pages, at last I found a great article

Odunlami says

Thank you, it is an helpful article.

seshu says

Good Explanation,

it was very Helpful to all,

Glory Kautuka says

thanks

A.Hemalatha says

very good notes. very helpful. thank u.

Rukdhar naij says

Thank you

Babayaro kabiru says

Am quite sure that these are extremely helpful article for both students and teachers, thanks.

Shwetabh Parasar says

It was well written in simple language.

Thanks

Freddie says

It has been such a helpful article it has surely helped me for my research

Sukanta says

It’s very easily understandable and well explained at the same time. Thank you.