Definition: Capital Expenditure or CapEx refers to the financial outlay made by the firm for an asset which is expected to stay in the business for a long time, so as to use the same for more than one financial year, which not only generates enduring benefits for the company but ensures the generation of revenue over the years.

In finer terms, when the company uses its funds for acquiring, improving or upgrading its long term assets, so as to increase its productivity, capacity and efficiency, such an expense is called as capital expenditure.

These expenditures can also be made with the aim of increasing the scope of operations, improving the working condition of assets or extending the useful life of the assets. Such expenditures are primarily made by the company to start a new unit, project or venture, with an aim of earning revenue therefrom.

Examples

- Overhauling expenses of second-hand machinery.

- Expenses made by the promoters before the commencement of business, i.e. preliminary expenses are of capital nature.

- Purchase of assets such as furniture, plant, building, computer, vehicles, etc. for the use in business and not for the purpose of trading and reselling.

- Trial run expenses of newly installed machinery.

- Advance paid in relation to a broadband connection, in the office.

- Fee paid for acquiring a license, to run a specific business.

Capital expenditure incurred by the firm for buying or upgrading the asset accrues long-lasting benefit to the firm and so the total amount spent on it will also be spread over the useful life of the asset.

Furthermore, the asset purchased by making capital expenditure can be reconverted into cash, irrespective of the fact that the reconversion resulted in profit or loss.

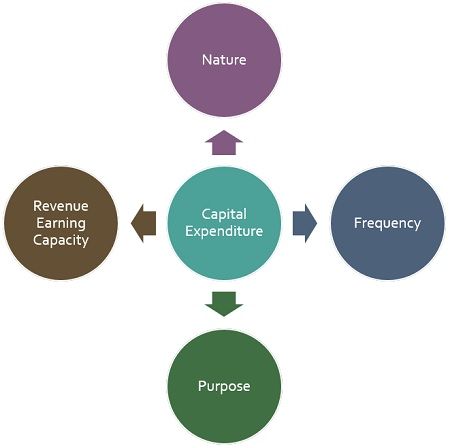

Factors Determining Capital Expenditure

There are certain factors on the basis of which the expenses are considered as capital expenditure, they are:

- Nature: The nature of the business, in which the company trades or deals plays a crucial role here, because, for a company engaged in real estate business, purchase of land or buildings is revenue expenditure, as it is considered as company’s inventory. But for other companies, the purchase of land and building will be a capital expenditure.

- Frequency: Capital Expenditure involves a one-time outlay of cash, usually nonrecurring in nature, and so it is not directly taken to Profit and Loss account, in the year in which the outlay is done. So, if an expense occurs frequently, it will be considered as an item of revenue expenditure and not a capital one

- Purpose: Expenditure made by the firm so as to increase the productive capacity of an asset will be regarded as a major repair, and so it is of capital nature.

- Revenue earning capacity: Any expenditure will be called as capital expenditure if it is made with the purpose of increasing the company’s earning capacity, as well as the benefits of such expenditure extends to a number of years.

Capital Expenditure is shown in the asset section of the balance sheet, as they generate revenue to the company, for more than one accounting year.

Further, these expenses are transferred to the company’s profit and loss account (income statement) of the year, as per the utilization of that benefit, from the expenditure, in the concerned accounting year.

Lewis Mbayi says

Am happy with the content am getting from you guys and it’s really enlarging my point of view