Definition: In business terminology, goodwill is the monetary worth of the advantage which a firm possesses over the other firms in the market with respect to profits which are expected to be derived in future over and above the normal profits.

As the time goes by, a business develops a good reputation, name, strong connections and a heavy customer base in the market, which helps it to earn excess profits, as compared to the profits earned by the similar firms operating in the industry, then such an edge over other is called goodwill.

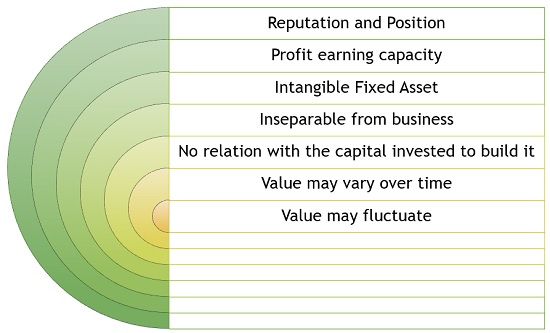

Salient Features of Goodwill

The basic features of goodwill are given below:

- Goodwill shows the overall reputation and position of the firm in monetary terms.

- It reflects the profit earning capacity of the enterprise.

- It is an intangible fixed asset, i.e. it cannot be seen or touched, but it can be felt, however, it is not a fictitious asset.

- It is associated with the business and so cannot be segregated like other assets which can be sold.

- It has no connection with the capital contributed to creating goodwill.

- Value of goodwill may change over time.

- Its value may fluctuate, due to various factors present in the business environment.

Goodwill is calculated by deducting the fair market value of all the identifiable assets and liabilities assumed, from the purchase consideration. The remaining amount will be the goodwill of the firm.

Factors Contributing to Goodwill

Goodwill is not created in one day, rather it takes years to acquire as well as great efforts are needed to maintain it. The factors that add to the company’s goodwill are:

- Quality of products or services offered

- Customer service

- Reputation of the founders or promoters.

- Managerial Efficiency

- Locational Advantage

- Monopolistic nature

- Consistency in dealings

- Competition

- Market share

- Reach or Coverage

- Marketing or Advertising Strategy

- Possession of a distinctive patent and trademark

- Customer Satisfaction

Goodwill is the likelihood that the customer would stay loyal and come again to the same place in future. So, it can be said that it is a business’s potential to earn surplus profits in the coming time.

Need for Valuation

The valuation of the goodwill of a business often arises when there is any major change in the business. The main reasons for its valuation are:

- Economic Damage Analyses: If the breach of contract or tort is suffered by a business enterprise, then it is valued to know the reduction in the value of the firm’s goodwill because of such breach.

- Amalgamation: When there is a merger of two business houses or one company’s business is acquired by another company, then also the goodwill is valued.

- Business Separation: When a business’s assets are separated, to individual business owners such as partners of a firm. So, it is a common measure to allocate the assets to the individual partners in the proportion of the relative worth of the assets built by each partner along with goodwill.

- Change in partnership: When there is admission, retirement or death of a partner in a partnership firm, goodwill is calculated, as the change in a partnership may affect the profitability of the partners.

- Business Enterprise Valuation: In asset-based approach, the company’s goodwill is identified and quantified, for the purpose of taxation, ownership transition, litigation, financing, corporate governance, bankruptcy and so forth.

There are various other reasons also in which goodwill of the firm is valued such as solvency test, insolvency test, bankruptcy and reorganization, intercompany transfer price, etc.

Leave a Reply