Definition: Zero-based budgeting or ZBB, is an emerging budgeting technique, which is introduced with the aim of coping with the demerits of the traditional budgeting system. Zero-based budgeting is different from the incremental (conventional) budgeting system in the sense that the former begins with a zero base, i.e. from a scratch and are not based on previous trends.

In traditional budgeting, previous year’s figures of expenditure are considered, whereas zero-based budgeting works on the assumption that the budget for the following year is zero till the requirement for a process, project, function, or activity is not confirmed for each penny, right from the first penny incurred.

Simply put, Zero-based budgeting is that form of budgeting wherein each cost element for the period is clearly justified, in terms of cost benefits. The management analyses and prioritizes the activities, depending on the determinants like alignment with the organizational objectives, fund availability, etc.

Hence, all the activities are reassessed every time the budget is prepared. Its aim is to reduce the expenditure, by identifying the areas where cost can be cut.

Characteristics of Zero Based Budgeting

- Focus of efforts is on both ‘how much’ a unit will incur and ‘why’ it is incurred?

- Decisions are based on what each unit can offer at the given cost.

- Individual unit’s objectives are aligned with the corporate objectives.

- Instant adjustments in the budget are possible if required.

- All the levels of the organization participate in the process of decision making.

It must be noted that zero-based budgeting technique is purely based on activities, wherein the budget is prepared for every activity, instead of a functional department.

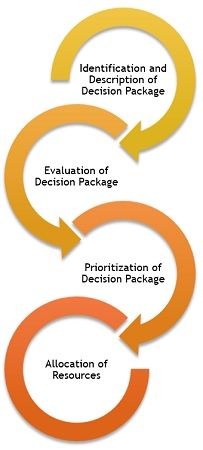

Stages of Zero Based Budgeting

To understand the stages of ZBB, first of all, you need to know the meaning of decision packages. Decision packages refer to the development of an operational plan for the activities for which decisions are to be made. The stages are given as under:

- Identification and Description of Decision Packages: Decision package ascertains a particular activity, so as to analyse and rank the activities against other activities, with respect to the use of scarce resources and make decisions thereon.

- Evaluation of Decision Packages: After identification and description, decision packages are evaluated considering the factors like alignment with the organizational objectives, regulatory requirement and availability of money.

- Prioritisation of the Decision Packages: Decision packages are ranked on the basis of activities.

- Allocation of Resources: Once the ranking is done, resources are allotted to the packages, which facilitates in the process of preparation of the budget, as it is done for the very first time, without any consideration to previous year’s budgets.

The decision packages provide you with the details such as the cost involved, return, objective, expected outcome, alternatives available and consequences of non-performance of the activity.

Superiority of Zero Based Budgeting over Traditional Budgeting

Zero Based Budgeting uses a scientific technique for evaluating various activities, which certifies that the activities carried out are relevant for the accomplishment of objectives. In addition to this, cost-benefit analysis is performed by the management, before allocating the resources to different activities. Moreover, excessive and unnecessary expenditure on various activities is identified and eliminated.

Lastly, it facilitates the implementation of Management By Objectives (MBO), by involving all the levels of the organization in the process of decision making.

Madou Zoulo says

thank you excellent