Definition: Activity Based Management (ABM) can be understood as the cost management implementation of activity-based costing. It is a management approach that concentrates on efficiently and effectively managing the activities so as to improve the quality of goods and services offered to the customers and also increase the profitability and competitiveness of the organization.

ABM uses Activity Based Costing as a tool for controlling costs at the activity level. Activity-based costing is a system that stresses on the activities which are carried out for producing products.

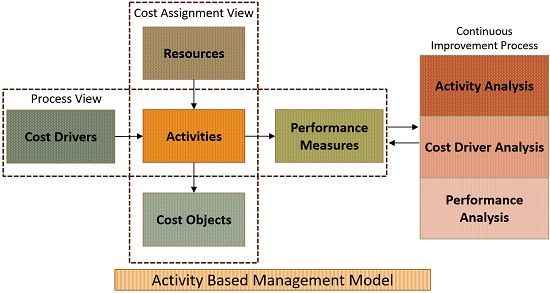

Activity Based Management Model

- Cost Driver Analysis: For the purpose of managing the activity costs, the factors that result in the activities to take place are to be identified.

- Activity Analysis: Activity Analysis is all about finding out the activities of the organizations and its centres, that are ought to be utilized in the activity-based costing. Based on the costs and benefits of the alternatives, the activities are divided into the number of activity centres. Further, it ascertains value added and non-value added activities:

- Value Added Activities: The activities which are very essential for the completion of the process are categorized as value-added activities.

- Non-Value Added Activities: Those activities which are not having any worth for both external or internal customers are termed as Non-value added activities. Indeed these activities do not enhance the quality of the product rather they have a negative impact on the cost and prices of the product or services as they create wastes, delays, increase the overall value etc.

- Performance Analysis: It involves discovering a proper measure to analyse the performance of the activity centres.

Activity Based Management aims to manage the organization with these analysis and also ascertains what directs the firm’s activities and how they can be improved.

Application of ABM in Business

- Cost Reduction: Activity-based management facilitates the organization to identify the costs against activities to determine the ways to reduce costs and even eliminate the entire activity if it is not adding any value to the products.

- Activity-Based Budgeting: ABB supplies a framework for forecasting the input required as per the budgeted level of activity. A comparison is made between actual results and estimated results to outline the activities with a high level of variances from the budget for a probable reduction in the supply of inputs.

- Business Process Reengineering: It entails examining and redesigning the processes and workflows of the organisation for improving the performance and also gaining excellence in business operations. It involves making significant changes regarding the way in which organisation operates currently. ABM helps in improving the business process efficiency and effectiveness.

- Benchmarking: Benchmarking is the process of making a comparison of the products and services offered by the company with that of the other organisations. It aims at identifying the ways to improve products and services of the firm.

- Performance Measurement: Nowadays, most of the firms concentrate on activity performance by observing the efficiency and effectiveness of activities, so as to compete successfully in the market.

ABM is not just an approach but also a management philosophy, that is oriented towards planning, implementation and measurement of business activities. It helps in cost reduction and also provides a proper basis for management decision making.

Leave a Reply