Definition: Buy Back of Shares, or Share Repurchase is a corporate move wherein a company purchases its own outstanding shares from the current shareholders. This buyback takes place at a higher price than the actual market price. Further, the motive behind this is to reduce the number of shares present in the open market.

When the company repurchases shares, cancellation of such shares is a must. Buyback of shares for the purpose of investment is not permissible.

With buyback, the outstanding shares on the market decrease. Therefore, it results in an increase in the proportion of shares that the company owns. So, the ownership stake of the existing shareholder’s increases. Also, there is a decrease in the company’s share capital.

Modes of Buy Back

- Tender Offer: Presentation of a tender offer to shareholders by which they get the alternative to submit either a portion or all of their shares within the given time frame. This alternative is available at a premium to the existing market price. Further, the premium is to compensate the investors for tendering (submitting) shares instead of keeping them.

- From the Open Market: The company repurchases shares on the open market over a long time span. It is possible through the book-building process or stock exchange.

- From Odd lot holders

- By purchasing securities issued to employees under ESOP (Employee Stock Option) and Sweat Equity Shares.

Sources of Buy Back

Buying of own shares and other specified securities out of:

- Free reserves of the company, e.g. general reserve, reserve fund, credit balance of Statement of Profit and Loss Account or

- Securities Premium Account or

- Proceeds of the issue of any shares or other specified securities.

Reasons for Buy Back

The company initiates the buyback of shares because of the following reasons:

- Improving earnings per share

- Improving return on capital, and return on net worth.

- Offering an additional exit route to the shareholders if the shares are undervalued or not actively traded in the share market.

- Preventing unrequested takeover bids.

- Returning excess cash to shareholders.

- Attaining optimum capital structure.

- Increasing the market value of remaining shares in the market as there will be a reduction in supply. This automatically increases the demand for the company’s shares.

- Preventing other shareholders from owning the controlling stake in the company.

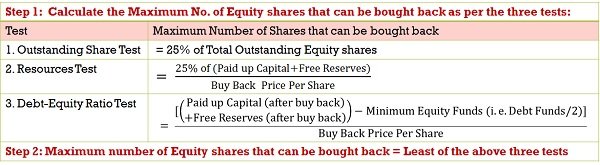

Calculation of Maximum Number of Shares that can be Bought Back

Conditions of Buy Back

- Authorization by Articles: The articles of association (AOA) of the company permits it to do so.

- Resolution: The company passes a special resolution on this, in the general meeting.

- Fully paid up shares: Shares of the company are fully paid up.

- Percentage: The buyback should not be more than 25% of the total paid-up capital and free reserves of the company.

- Debt-Equity Ratio after buy-back: Post-buy-back, the ratio of debt that the company owes should not exceed twice the capital and free reserves. In short, the debt-equity ratio after the buyback should not be more than 2:1. Nevertheless, the central government can determine a higher limit in specific cases.

- Time Limit: Within 12 months from the date of passing the special resolution at AGM, the buyback should be complete.

- SEBI Regulations: Buy Back of shares are listed on any recognized stock exchange. Further, it should be as per the regulations made by the Securities Exchange Board, in this context.

- Destroy: The shares or securities bought under this process need to be destroyed physically. This must take place within seven days from the last date of completion of buyback.

- Restriction on the further issue: Company cannot make a further issue of the same kind of shares or securities within 6 months. However, it can issue:

- Bonus shares

- Sweat equity shares

- Under ESOP

- In place of conversion of warrants or preference shares or debentures into equity shares.

- Buy Back not Allowed when: Company cannot purchase its own shares or other specified securities directly or indirectly by way of:

- Any subsidiary company (including the company’s own subsidiary)

- Any investment company or its group

- Or any company which has failed to pay interest, deposit, dividend, term loan, redemption amount of preference shares or debentures and so forth, is subsisting.

- Explanatory statement: Notice of General Meeting which company issues must include an ‘Explanatory Statement’ containing:

- Complete disclosure of material facts

- Need for buyback of shares

- Class of securities which the company intends to buy back

- The amount which the company will invest under this process and

- The time limit for its completion

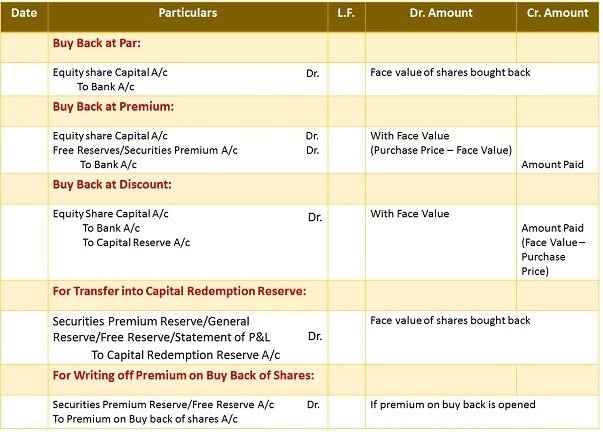

Journal Entries for Share Buy Back

Points to Remember

- The company can buy back only fully paid-up securities. If the securities are partly paid up, then they should be made fully paid up by making the final call.

- A sufficient balance should be available in the credit of free reserves when the company intends to buy back shares out of it.

- An amount equal to the face value of the shares repurchased, from free reserves must be transferred to Capital Redemption Reserve. When the premium is paid, it is adjusted against free reserves or securities premiums.

- Discount on buyback needs to be transferred to Capital Reserve Account.

- Capital Redemption Reserve (CRR) needs to be utilized to issue fully paid bonus shares.

A word from Business Jargons

Buy Back of shares means purchasing of own shares by the company. This is to cancel the shares when the company is having surplus cash than it requires.

Leave a Reply