Definition: Single Entry System, is the oldest and most straightforward method of keeping records of financial transactions, which is rarely prevalent these days. In this system, only one side of the transaction is recorded, because of the absence of any prescribed rules and so the records maintained are more or less incomplete.

In a nutshell, single entry system of bookkeeping lacks the duality concept and so the financial transactions are recorded only once and not in their two-fold aspects, as debit and credit.

Characteristics of Single Entry System

- Maintenance of Cash Book: Cash Book is prepared and maintained, in which both business and personal transactions are included.

- Personal Accounts: Only personal accounts are created and maintained, whereas the real and nominal accounts are not given due weight, in this system.

- Original Vouchers: Under this system, original vouchers play an important role, as they help in gathering information about the date of transaction, amount, parties, discount (if any) and so forth.

- Final Accounts: In Single Entry System, it is quite difficult to prepare final accounts, due to unavailability of nominal and real accounts. So, to prepare the financial statement, the available information is analysed and converted into a double entry system, by determining the missing figures, after that Trading and Profit & Loss Account is prepared. Further, the figures of assets and liabilities are calculated from the information at hand, but they are also estimates. Hence, the Statement of Affairs is prepared in place of the Balance Sheet.

- Profit or Loss: Profit earned or loss sustained is estimated, out of the information available and so exact profits is not ascertained.

- Suitability: The system is appropriate for small businesses, like sole proprietorship business and partnership firms, as they maintain records of cash and credit transactions only.

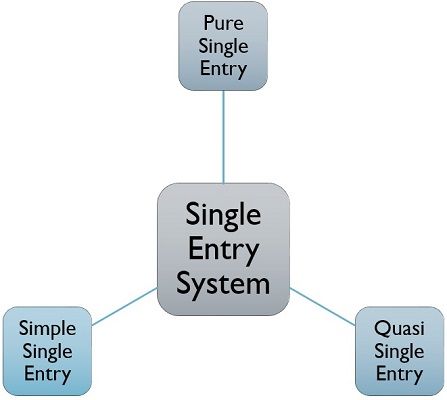

Types of Single Entry System

- Pure Single Entry System: In this method, only the personal accounts are maintained and there is no information present, concerning the sales and purchases, cash in hand, and bank balance.

- Simple Single Entry System: In a simple single entry system, cash book is maintained along with the personal accounts and these are maintained as per double entry system of bookkeeping. Cash received or paid, from/to business debtors or creditors are merely written on the bills issued or received.

- Quasi Single Entry System: In this system, subsidiary books such as sales book, purchases book, bills receivable book and bills payable book are maintained in addition to cash book and personal accounts.

Single Entry System is simple and easy to maintain as it does not need any professional accountant to keep the records up to date. And so this system is quite helpful for small businesses and trades operated solely by individuals. Further, the system is quite economical.

Limitations of Single Entry system

It is an unscientific method of keeping business records because it does not follow the duality concepts (meaning that every transaction affects two sides). Profit or loss ascertained and reported are simply estimates, which cannot be considered as actual and accurate, because of not maintaining real and nominal accounts.

Moreover, it is not easy to detect frauds and errors (if any). The firm may also face difficulties in raising loans because the banks and financial institutions cannot rely on financial information provided by the entity. Due to this very reason, this method is not adopted by companies, and they have to maintain their books of accounts as per the Companies Act,

Doris Senesie says

Thank u I enjoy reading the note