Definition: Consignment implies a trading arrangement, wherein one party transfers goods to another party without immediate payment, who agrees for selling them on behalf and at the risk of the former, as per the instructions, to the customers, for a commission as a percentage of revenue from the sale proceeds.

Consignment is opted when the owner of the goods does not have any branch in a specific area or place.

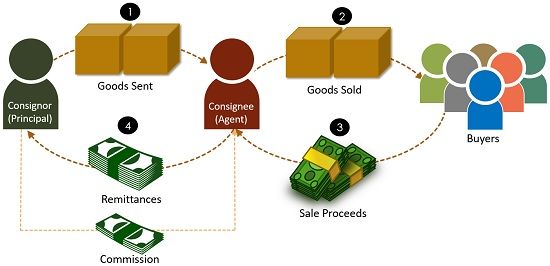

The person who transfers the goods is called consignor, whereas the person to whom the goods are transferred is the consignee. The relationship between the consignor and consignee is that of principal and agent, and not of a buyer and seller, whereby consignor acts as principal and consignee is the agent.

The consignee is entitled to pay to the consignor for the goods when the sales take place. If there is any unsold stock and the term of the agreement expires, then it will be returned to the owner of the goods, i.e. the consignor.

Process of Consignment

Let’s understand the process of consignment with the help of figure:

Characteristics of Consignment

In consignment, the consignor appoints another person as his agent (consignor) to sell the goods, against which he/she receives a commission. Upcoming points will present the main features of consignment:

- The ownership of the goods remains with the principal, i.e. consignor, and only the possession is transferred to the agent, i.e. consignee.

- The goods which are transferred, sent or dispatched is called consignment.

- All the expenses incurred in connection to the consignment are borne by the consignor only.

- The consignee will not be held liable for any damage to the goods during transit.

- All the risk and reward associated with the consignment belongs to the consignor only.

Any sale proceeds received thereon is remitted to the consignor, after deducting the expenses (such as advertisement expenses, selling expenses, godown rent, loading/unloading charges, etc) and commission.

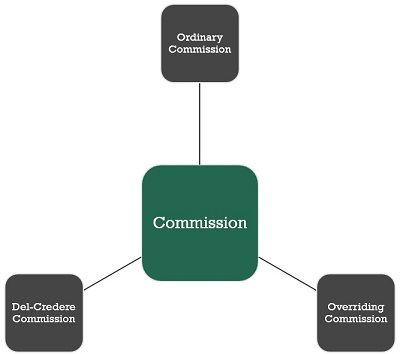

Commission

Consignee is entitled to a commission for the sales made on behalf of the consignor which is calculated as per its nature. There are three types of Commission paid in case of consignment:

- Ordinary Commission: The consideration payable to the consignee, by the consignor for the sales made, when the consignee is not responsible for bad debt which may arise. It is calculated as a percentage of gross sales.

- Del-Credere Commission: It is the extra commission which is payable to the consignee when he takes the responsibility for collecting money from the customers to whom goods are sold on credit. Further, if the customers refuse to pay the amount, the consignee bears the loss of bad debts. It is calculated on total sales and not on credit sales unless otherwise specified.

- Overriding Commission: It is a special commission payable to the consignee when he sells the goods on the excess of sales price over the invoice price.

Proforma Invoice

The consignor sends the proforma invoice of the goods consigned. A proforma invoice is a statement which is used to provide information as to the particulars of the goods sent to the consignee.

Account Sales

Account sales are sent by the consignee, which carries all the details related to the sales made by the consignee, expenses incurred, goods destroyed in transit, a commission earned by the consignee, and balance due to the consignor. If any advance is made by the consignee in the form of cash or bills of exchange, then the same will also be adjusted against the proceeds received from the goods sold.

In the books of the consignor, three accounts will be prepared – Consignment Account, Goods sent on Consignment Account and Consignee’s Account. However, in the books of Consignee, Consignor’s Account will be created.

Leave a Reply