Definition: Preference Shares refers to the shares that possess preferred position over other classes of shares, i.e. equity shares, as to the payment of dividend and repayment of capital, when the company goes to liquidation.

The dividend to preference shareholders is either paid at a certain amount or at a certain rate. Further, the shareholders have no right to attend and vote at the Annual General Meeting of the company, as possessed by the equity shareholders.

The money raised by the company by issuing preference shares is called as preference share capital. The cost of capital of a preference share is less than equity shares but higher than debentures because interest paid on debentures is a tax-deductible expense, but the dividend is not a tax-deductible expense.

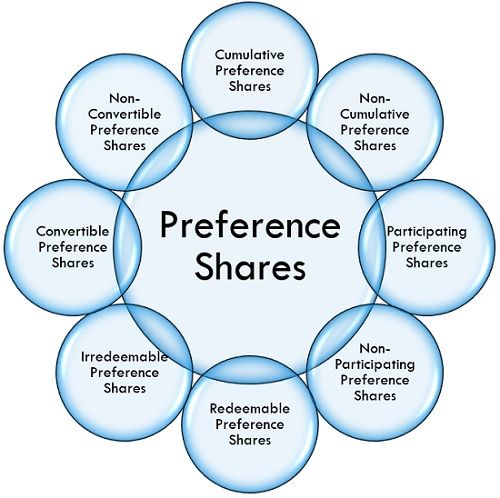

Types of Preference Shares

There are eight types of preference shares discussed as under:

- Cumulative Preference Shares: As the name itself signifies, these shares are entitled to a fixed amount or rate of dividend, which should be paid either out of current year’s profit or out of future profit if the current year’s profit not enough for the payment of dividend.Hence, if in a certain accounting year, the dividend is not paid to the preference shareholders then the dividend is carried forward to the next accounting year as arrears of dividend which appear as a contingent liability in the company’s balance sheet.

Further, if the company fails to pay dividend consecutively for two years than the holders get the right to participate and vote at the General Meeting of the company.

- Non-cumulative Preference Shares: Such shares possess only a fixed amount or rate of dividend. If the dividend for a particular financial year is not announced due to loss or any other cause, then dividend for that particular year expires, as it is not carried forward to the next year and hence remains unpaid.

- Participating Preference shares: This category of preference shares carries the right to participate in the surplus profits, left over after paying a dividend to the equity shareholders at a certain rate.Further, the shareholders are also entitled to receive a specified proportion of surplus, after the equity shareholders are paid off, at the time of winding up of the company.

- Non-Participating Preference Shares: The shares which are entitled to a fixed amount of dividend only, and there is no additional rights conferred to the shareholders are known as Non-Participating Preference Shares.

- Redeemable Preference Shares: The preference shares which are repaid at a fixed maturity date, or the discretion of the company are known as Redeemable Preference Shares. The repayment of the amount on these shares is called the redemption of shares.

- Irredeemable Preference Shares: The shares which are non-redeemable in nature are known as irredeemable preference shares. Such shares do not have an arrangement for redemption and the amount is repayable to the holders only at the time of winding up of the company.Further, no company is allowed to issue irredeemable preference shares or the preference shares which are redeemed after the stipulated term, i.e. 20 years.

- Convertible Preference Shares: As the name suggests, convertible preference shares are the ones which are convertible into equity shares, at the option of the shareholder, after the expiry of the specified term. So, they are also called as quasi-equity shares.

- Non-Convertible Preference shares: When the preference shareholder is not entitled to convert their holding into equity shares are termed as non-convertible preference shares.

Unless otherwise specified in the company’s Articles of Association, the preference shares issued by the company are non-cumulative, non-convertible, non-participating and redeemable in nature.

Further, According to Company’s Act, 2013 there is a prohibition on the issue of irredeemable preference shares. Hence, preference shares are issued for a specified period, after which the company redeems them.

As per shareholders point of view, preference shares are less riskier in comparison to equity shares as it gives regular income, in the form of a fixed dividend. However, the preference shareholders have no say in the management as they do not carry voting rights, which allows them to participate in the Annual General Meeting of the company.

Leave a Reply